2026-01

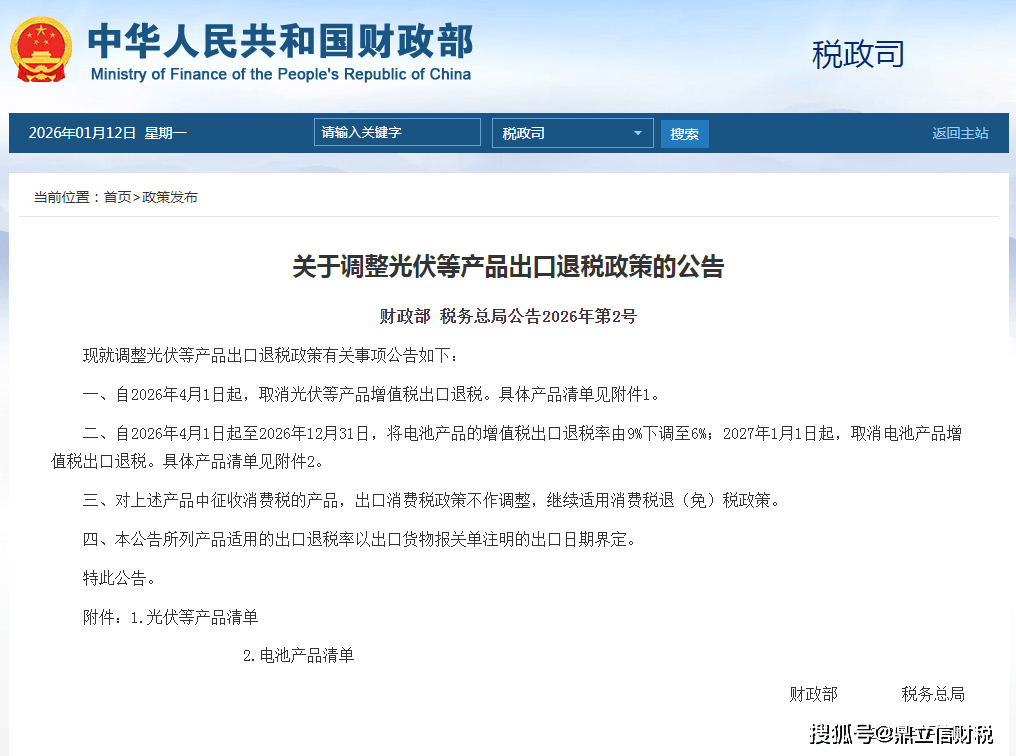

15On 8 January 2026, the Ministry of Finance and the State Taxation Administration jointly issued the Announcement on Adjusting Export Tax Rebate Policies for Photovoltaic and Other Products. This clarified that from 1 April, VAT export tax rebates for core photovoltaic products would be fully abolished. For battery products, a tiered reduction policy of ‘9% → 6% → 0%’ would be implemented, with rebates being completely phased out from 2027 onwards. This represents a significant adjustment following the November 2024 reduction of the rebate rate from 13% to 9%, marking the formal conclusion of China's photovoltaic industry's development phase reliant on export tax rebate subsidies. The policy implementation will exert systemic impacts across the entire photovoltaic supply chain and related enterprises, progressing from short-term cost shocks and mid-term industry consolidation to long-term industrial upgrading. This will propel the sector towards a profound transformation from ‘scale expansion’ to ‘value creation’.

Short-term impact: Steep cost increases trigger export rush, cash flow pressures test corporate resilience

The immediate repercussions of this policy adjustment manifest as rigidly rising export costs for enterprises and short-term export rushes, with the industry entering a three-month ‘window period of strategic manoeuvring’. From a financial perspective, the reduction of the PV product tax rebate rate from 9% to zero means that for every ¥1 million worth of products exported, enterprises will directly lose ¥90,000 in rebate income. This income was previously often leveraged by small and medium-sized enterprises as bargaining power to secure low-price orders. Industry calculations indicate that export profits for a single 210R-model photovoltaic module will decrease by 46-51 yuan, with export costs rising by approximately 4% per watt. For the photovoltaic sector, where the average gross margin of the main industrial chain stood at just 3.64% in the first three quarters of 2025, some low-margin enterprises may face immediate losses.

Cash flow pressures further exacerbate short-term operational risks. Export tax rebates form a crucial pillar of PV enterprises' cash flow. Taking leading firm JinkoSolar as an example, its outstanding export tax rebate receivables reached 913 million yuan in the first half of 2025. Following the rebate cancellation, enterprises not only lose this stable inflow of funds but also bear the cost pressure of transferring input tax credits. Fiscal case studies indicate that for photovoltaic module exports of comparable scale, post-policy implementation yields RMB 780,000 less in profits than exports during the window period, with a concurrent RMB 780,000 reduction in net cash inflows. Against this backdrop, the industry has witnessed a pronounced surge in export activity. Multiple suspended manufacturers have urgently resumed production, while some enterprises plan to operate continuously throughout the Spring Festival period, striving to complete customs declarations for exports before 31 March to secure the 9% tax rebate rate.

In contrast to the photovoltaic sector's blanket adjustment, the tiered reduction policy for battery products affords enterprises greater flexibility. During the transitional period from April to December 2026, when the rebate rate drops to 6%, enterprises like CATL and EVE Energy—where exports constitute over 40% of revenue—can gradually mitigate impacts by optimising cost structures and adjusting pricing strategies. However, they must complete core capability upgrades within nine months to confront the ultimate challenge of zero rebates in 2027.

Mid-term shakeout: Accelerated clearance of outdated capacity, markedly enhanced industry concentration

Policy adjustments will effectively resolve the industry's chaotic ‘low-price competition and subsidy spillover’ issues, accelerating supply-side reform. Since 2024, China's photovoltaic exports have exhibited a pattern of ‘increasing volume but decreasing price’. Some SMEs have directly passed on tax rebates to overseas buyers, undercutting prices to secure orders and sustain operations. This practice not only erodes domestic corporate profits but also substantially heightens risks of international trade friction. Following the rebate abolition, this loss-making competitive model will become unsustainable. SMEs lacking technological advantages, economies of scale, and bargaining power will be the first to exit the market.

Industry consolidation is an inevitable trend. Within the next 12 months, approximately 30% of SMEs lacking core competitiveness are projected to exit the market, with industry capacity utilisation rates expected to rebound from the current 50%-60% to a more sustainable level. Leading enterprises will capture market share through multiple advantages: firstly, economies of scale delivering unit cost advantages, enabling them to pass on over 90% of cost increases via price hikes; secondly, the ability to command product premiums through technological differentiation, with firms like LONGi and JinkoSolar already establishing competitive advantages through their N-type high-efficiency modules; thirdly, enhanced risk resilience through vertical integration, as companies such as Tongwei and JA Solar cover the entire value chain from polysilicon to modules, enabling internal synergies to absorb cost pressures. The industry's CR5 (concentration ratio of the top five firms) is projected to rise by 5-8 percentage points, shifting the competitive landscape from ‘price wars’ to ‘value wars’.

Impact varies across supply chain segments. The module segment, characterised by high export reliance and intense price competition, faces accelerated consolidation with significant survival pressures for SMEs. Supporting segments like wafers and mounting systems experience relatively milder disruption but will undergo capacity optimisation alongside broade